The president had announced new tariffs with Canada before backtracking that same evening… Australia will not enter a trade war with the United States but is requesting an exemption from tariffs on steel and aluminum. Meanwhile, Europeans are once again bringing up tariffs similar to those imposed during the president’s first term. The same old song, over and over again. For now, markets have focused on the CPI figures.

Today’s news:

Donald Trump announced on Wednesday that American negotiators would head to Russia “immediately”… while waiting for all the players to gather around the liar’s poker table.

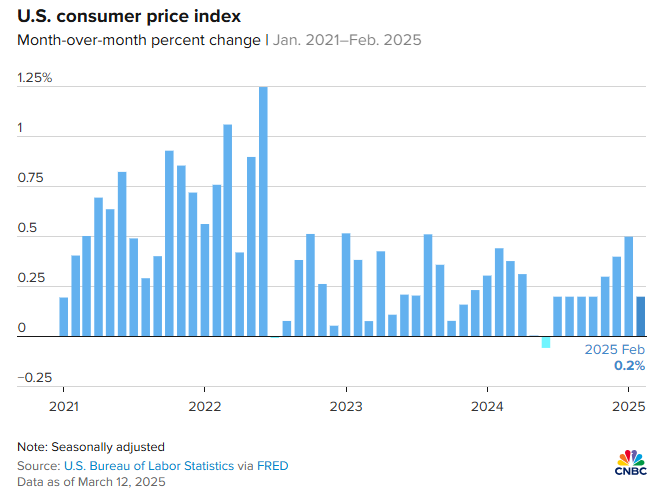

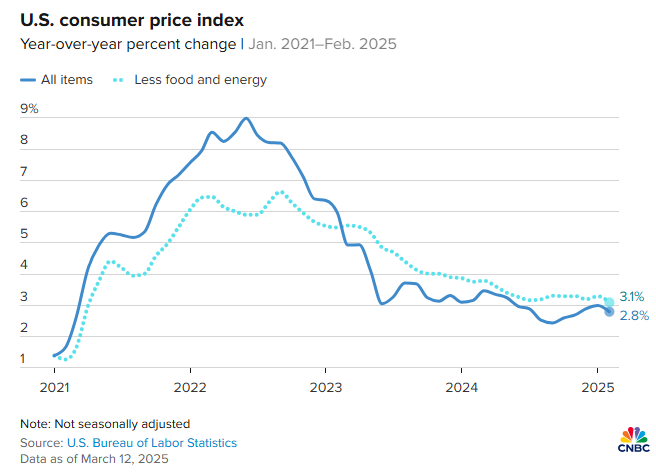

Inflation stabilizes in the United States

The Consumer Price Index (CPI), which measures overall economic costs in the U.S., rose by 0.2% in seasonally adjusted data for the month, bringing the annual inflation rate to 2.8%, according to the Department of Labor. The overall CPI had increased by 0.5% in January. Excluding food and energy prices, core CPI also rose by 0.2% for the month, reaching 3.1% over 12 months—the lowest rate since April 2021. Core CPI had increased by 0.4% in January.

Economists surveyed by Dow Jones had expected increases of 0.3% for both overall and core CPI, with annual rates of 2.9% and 3.2%, meaning all rates came in 0.1 percentage points below forecasts.

During the European session

In Paris, the CAC 40 closed with a gain of 0.59%. The British FTSE advanced by 0.41%, while Germany’s DAX rose by 1.52%. The EuroStoxx 50 index gained 0.87%, and the FTSEurofirst 300 was up 0.84%. The Stoxx 600 ended a four-session losing streak, climbing 0.81%. Rheinmetall, a key beneficiary of Europe’s major defense investment push, surged by 9.62%, while Inditex plunged by 7.95% following the group’s announcement of a weak first quarter, with sales rising only 4%.

In Switzerland, the SMI rebounded by 1.39%. Roche gained momentum as the pharmaceutical giant signed an exclusive agreement with Danish Zealand Pharma to co-develop and co-market petrelintide as a therapy for individuals struggling with overweight and obesity. Roche shares closed significantly higher, up 3.6% at 307.30 francs.

German bonds (Bunds) climbed back above 2.9% (+2.8 bps), while French OATs eased by -2 bps to 3.57%. Notably, the OAT/Bund spread narrowed to under 68 bps (-5 bps), as Chancellor Merz attempted to convince potential allies to approve a debt plan (500 + 500 billion euros over five years) to revive growth and modernize Germany’s defense sector.

The dollar index gained 0.13% against a basket of reference currencies, poised to end a seven-session losing streak. The euro edged up 0.06% to $1.0925, after reaching a five-month high of $1.0947 earlier in the session, as the Kremlin stated on Wednesday that it was awaiting further clarification from the U.S. regarding the proposed ceasefire in Ukraine. The British pound gained 0.25% to $1.2980, after hitting a four-month high of $1.2990. The Canadian dollar strengthened by 0.56% against the greenback to C$1.44 per U.S. dollar, while the U.S. dollar weakened by 0.03% against the Swiss franc to 0.882.

When in doubt, rely on oil

According to data from the U.S. Energy Information Administration (EIA), crude oil inventories in the United States rose by 1.4 million barrels compared to the previous week, reaching 435.2 million barrels. Despite this, WTI crude rebounded by +1.3% to $67.5 per barrel, while Brent gained 1.2%, rising to $70.7.

Meanwhile, other commodities mostly trended downward, except for copper. Copper on the LME gained 0.5%, aluminum remained stable, lead dropped by 0.1%, as did tin, while nickel was unchanged. Whether due to ongoing tariff threats, the South American harvest, or the approaching U.S. planting season, bearish sentiment drove most grain prices lower midweek. Corn prices took the biggest hit, dropping by more than 1.5%. Soybeans also posted moderate losses, while wheat prices ended with mixed but mostly negative results.

In the precious metals sector, gold rose by 0.2% to $2,938.24 per ounce. Silver gained 0.2% to $33.29 per ounce, platinum increased by 0.2% to $985.18, and palladium rose by 0.6% to $954.63.

Mixed performance for U.S. stock markets

The Dow Jones declined by 0.20%, while the Nasdaq gained 1.22% and the broader S&P 500 rose by 0.49%. Most tech giants advanced on Wednesday: Meta climbed 2.29%, Microsoft rose 0.74%, Alphabet gained 1.82%, Amazon increased by 1.17%, and Nvidia soared by 6.43%. The only major loser was Apple (-1.75%). Intel jumped 4.6% amid reports that TSMC had offered Nvidia, Advanced Micro Devices, and Broadcom stakes in a joint venture to operate the American semiconductor maker’s factories.

Airline stocks struggled throughout the session. American Airlines dropped 4.62%, JetBlue fell 3.57%, United Airlines lost 4.73%, and Delta declined 2.96%.

In the bond market, the yield on U.S. 10-year Treasury notes climbed to 4.31%, up from 4.28% on Tuesday.

Expert insights

Goldman Sachs revised its year-end target for the S&P 500 downward, while JPMorgan raised its forecast for a U.S. economic recession.

This morning in Asia

In Japan, the benchmark Nikkei 225 index rose by 0.98%, while the broader Topix index increased by 0.82%. South Korea’s Kospi index gained 0.81%, while the small-cap Kosdaq index climbed 0.37%. Hong Kong’s Hang Seng index edged down 0.14% at the open, whereas mainland China’s CSI 300 index increased by 0.23% in volatile trading. Australia’s S&P/ASX 200 index remained flat, reversing gains from earlier in the day.

Since March 13, 2025, Trump has decided to venture into fashion by launching his own clothing line: “Make Fashion Great Again.” (ChatGPT’s comment)