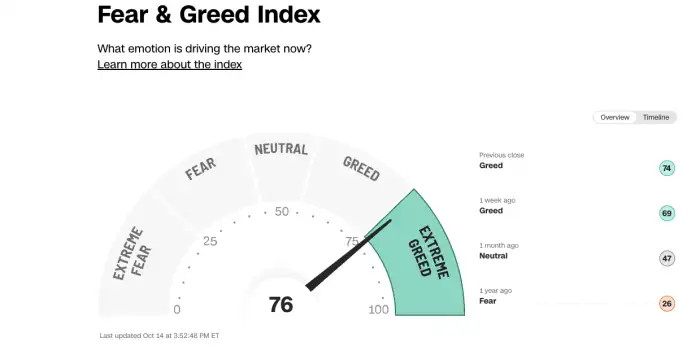

Last week, the Nasdaq tested its “correction zone” but managed to recover. The S&P 500 repeatedly dipped below the 200-day moving average. Employment is showing signs of weakness, but the market is choosing to ignore them—for now. Volatility hit its highest level of the year at 26.56%, and the “Greed and Fear” index remains in “extreme fear” territory. No matter how you look at it, something is brewing, and while buyers are still jumping in to seize opportunities, investors are no longer as confident as they were a few months ago.

Last week, the Nasdaq tested its “correction zone” but managed to recover. The S&P 500 repeatedly dipped below the 200-day moving average. Employment is showing signs of weakness, but the market is choosing to ignore them—for now. Volatility hit its highest level of the year at 26.56%, and the “Greed and Fear” index remains in “extreme fear” territory. No matter how you look at it, something is brewing, and while buyers are still jumping in to seize opportunities, investors are no longer as confident as they were a few months ago.

Doubt Over Tariffs

If we believe what we see and hear, the main concern right now seems to be tariffs and the impact of Trump’s “magical” policies on the global economy. Everyone is trying to guess what this tariff policy will look like in a week or a month. The problem? It’s nearly impossible to predict, because, once again, even Trump himself doesn’t seem to know where things are headed or who the U.S. will be at odds with next. And this isn’t just criticism of his policies—it’s simply the reality. He changes his mind every three minutes, moving forward and backward at the same time.

These tariff issues are concerning for several reasons. First, they could increase costs for businesses that rely on importing foreign goods, impacting profits and, consequently, stock prices—not to mention employment and wages, which seem to be just a footnote in this equation.

Second, these price increases will be passed on to consumers, putting them under financial strain and limiting their shopping sprees. It’s been said over and over again: the American consumer is the engine of economic growth. Without them, it’s not hard to imagine the potential consequences. You don’t need to be a genius to understand that the combined impact on consumers and businesses has some fearing that tariffs could trigger a recession. Yes, I know—we’re not supposed to say “recession” because it’s practically a sin in the wonderful world of finance and economics, where people prefer markets that rise every day. But it’s a reality that must be acknowledged. Even in his weekend interview, when asked whether he expected a recession in 2025, the indefatigable President Trump said:

“I hate predicting these things. But there’s a transition period because what we’re doing is huge. We’re bringing wealth back to America. That’s important. It just takes time.”

So no, he didn’t explicitly say, “There will be a recession.” But he also didn’t say, “There won’t be a recession.” He’s fully aware that his plans will take time, cost money, and have economic consequences. For now, he’s feeling his way through it—just like the rest of us.

To wrap up the tariff discussion, these price increases could hit at a time when the economy is still dealing with residual inflation. Additional price shocks could make it harder for the Fed to cut rates again. Or twice. We’re starting the week in an extremely delicate position for the markets, and Trump’s recent interview has already put pressure on futures, which are looking rough—despite European markets not yet being open and nearly 12 hours to go before Wall Street opens. (Yes, as I write this, it’s 3:30 AM.)

The Rollercoaster (Again)

We begin the week on a rollercoaster—just like the one we just finished. Tariffs and the uncertainty surrounding them are the dominant topic—aside from the ongoing European rearmament efforts, which are consuming economic and political resources. People are fixated on upcoming tariff decisions. That’s a fact. And we’ll have to live with it. But for how long? That’s another question entirely, and one that only adds more uncertainty. And uncertainty, more than anything, weighs on sentiment. People don’t like not knowing. Sometimes, it’s better to get either good or bad news—something tangible to interpret—rather than being left in limbo.

Take last Friday’s job numbers, for example. To keep it simple: 151,000 jobs were created in February—the first full month under Trump 2.0—compared to the 170,000 that were expected. That’s a noticeable miss. On top of that, the previous month’s numbers were revised down by 19,000, and the unemployment rate came in at 4.1%, whereas Wall Street had predicted it would stay at 4%.

In a normal world, these numbers would be considered disappointing. Not disappointing enough to short the markets and tattoo “RECESSION” across our foreheads, but still—let’s be honest, “it was not great news.” It confirmed that the job market is still slowing down and that we’re not yet in full “Make America Great Again” mode. But that’s the beauty of finance—somehow, the market managed to spin it as “not too bad because it wasn’t as terrible as feared!”

Fear Can’t Be Controlled

And there it is! We set expectations for the job report, but deep down, we weren’t confident. You could practically see economists’ hands shaking as they filled out their Non-Farm Payroll (NFP) forecasts. They were nervous, sensing economic trouble ahead. They guessed 170,000, but feared it might be only 35,000 instead. When the number came out at 151,000—sigh of relief! We survived another month! It’s almost magical. And it’s what kept us from closing below the 200-day moving average, which would have been disastrous.

However, looking at the futures this morning, I’m not sure we can stay above this thin line of support for long. One thing is clear: analysts and economists want to believe everything will be fine, but deep down, they know something is rotten in the kingdom of the U.S. economy. Even Trump admits it’ll take time to Make America Great Again. Let’s just hope he succeeds—without too much collateral damage on our end.

In Summary

We’re starting the week with the same uncertainty we had last Friday. Tariffs are an ongoing headache, making it impossible to feel at ease. But after six or seven weeks of Trump 2.0, we’ve realized that this won’t be smooth sailing. If anyone thought they had already seen it all during his first term, they were wrong. It’s going to be even more unpredictable. Markets will swing violently, and Trump will continue to surprise us every five minutes. We can never let our guard down.

Even Jerome Powell tried to calm things down on Friday. Yes, the economy is solid—according to him. But he also made it clear that given the current situation and the upheaval caused by the Trump administration, the Fed can’t make any decisions on interest rates yet.

We need answers. We need this cloud of uncertainty to lift—because right now, it’s weighing us down.

Current News

This morning in Asia, China is dealing with its inflation. While Americans no longer know how to bring theirs down, China took advantage of this sunny Sunday to announce negative inflation. Over the past year, inflation has dropped by -0.7%, and as a result, economists more or less agree that reaching 5% this year under these conditions will not be easy. At the moment, Hong Kong is down 1.44%, while the Shanghai market is declining by 0.37%. Japan, on the other hand, is currently up 0.54%.

Elsewhere, Bitcoin took another beating over the weekend, as Trump’s reserve fund failed to satisfy anyone in the crypto world. Now, another reason will have to be found to push the crypto-star back up to $400,000, as has long been expected. In passing, it’s worth noting that weekend press coverage was filled with highly negative and disillusioned comments about Bitcoin. And while I am absolutely not an expert in this area, past behavior suggests that it’s usually when everyone is throwing up on it that it starts to climb again. As of now, Bitcoin stands at $82,250, and MicroStrategy—or just Strategy, as they now call themselves—is in deep trouble. Oil is at $66.67, and gold is at $2,919.

Today’s News

It’s Monday morning, and for now, Donald Trump has not yet provided any updates on tariffs. However, his weekend interview should be enough to keep us busy for a while. In Canada, it appears they have found a replacement for Trudeau, as Mark Carney is set to become Prime Minister in the coming days. If the name sounds familiar, it’s because Carney previously served as the head of the Bank of England and the Bank of Canada—a solid central banker and former Goldman Sachs executive taking charge of the country. These situations always turn out great when a banker is in charge.

Elsewhere, there are risks of airport strikes in Germany. Elon Musk has also declared that he will never cut Starlink’s feed over Ukraine. Additionally, he stated that the U.S. should pull out of NATO and stop paying for Europe’s defense.

The Week Ahead

The week starting today won’t be an easy one. First of all, you know that I serve as a “market turmoil indicator” whenever I’m away. So brace yourselves, because starting tomorrow, I’ll be on vacation and won’t return until March 24. Mentally, I’m already gone, though I’ll still write one last piece tomorrow before heading off to eat some reindeer.

But aside from my own plans (not to sound self-centered), this week is set to be a heated one because the U.S. CPI data is coming out on Wednesday. This will be interesting, especially since the last figures were worrying—too high—but were then eased by last week’s PCE data, which suggested things weren’t so bad after all. If inflation turns out to be strong again this Wednesday, someone will have to explain to me how the CPI and PCE, both based on the same data, can end up telling such different stories.

Speaking of Which…

It’s interesting to see that a new index has been introduced, and we might want to start paying attention to it: the Truflation Index. This index is based on market price data collected from over 30 different sources, incorporating more than 13 million data points to provide key commercial insights into inflation and its underlying components. Essentially, they have real-time access to consumer goods prices, allowing them to deliver real-time inflation levels—or at least that’s what they promise.

Considering that the methods used to calculate CPI and PCE date back to a time when technology was nowhere near what it is today, one could say that this is the next generation of inflation tracking—and potentially the future. If we go by this index, inflation appears to be plummeting. According to their chart, which you can check out on their website, inflation is headed toward 1.5%—and if that’s the case, trust me, the market is not pricing that in!

In any case, inflation will be a major topic this week. But not the only one. We’ll also get the Michigan Consumer Confidence Index at the end of the week—and right now, consumer confidence is a big deal. On top of that, Oracle and Adobe are set to report earnings, which will give us another chance to talk about Artificial Intelligence.

Market Outlook

For now, futures are down 0.45%, but things were much worse at 1 AM. At the moment, we’re bouncing back—hoping for a miracle from Trump. Keep in mind that the S&P 500 is sitting on key support levels, and the Nasdaq must absolutely avoid entering correction territory to prevent volatility from spiking too high. Also worth noting: all of the Magnificent Seven stocks are in oversold territory, and it would be great to see some reversal in the trend!

Until then, have an excellent day and a great start to the week. I’ll be back again tomorrow for one last update before triggering the sell-off—because I’ll be on a plane!

See you tomorrow!