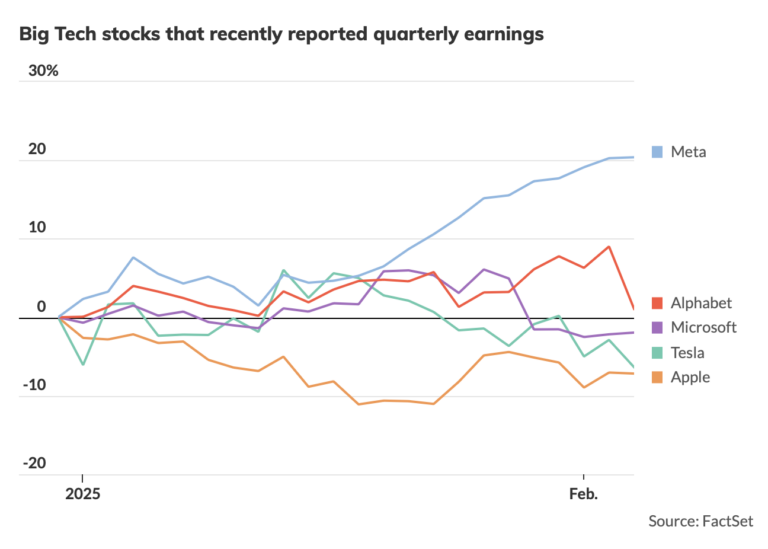

As we approach the end of this second week under Trump 2.0, if there’s one thing to take away, it’s that the market is showing an absolutely impressive level of resilience. I’m not sure whether to use the word resistance or resilience—either way, the relative strength of global markets is striking. After facing the DeepSeek attack on AI, followed by the aggressive tariff measures earlier this week, one might have expected far worse. Just yesterday, the “relatively” poor results from Google and AMD had put the market in a tricky position. But not at all—once again, investors managed to sort things out.

Tariffs Still Weigh on Europe

As we approach the end of this second week under Trump 2.0, one thing is clear: the market is demonstrating an absolutely impressive level of resilience. I don’t know if we should use the word “resistance” or “resilience”—either way, the relative strength of global markets is striking. After enduring DeepSeek’s attack on AI, followed by the vicious tariff assault earlier this week, we could have expected much worse. Just yesterday, the “relatively” poor earnings reports from Google and AMD put the market in a tough spot. But no—investors managed to sift through the data once again.

When looking at where indices closed yesterday, the picture is quite encouraging, considering the fears still looming over us—fears that will last for another 3 years, 11 months, and two weeks. We’ve understood that as long as Trump is in office, we will live under the constant threat of him getting angry about something. And right now, he is very, very angry. But despite these tensions, as well as the “bad numbers” from some major companies that make up a large portion of U.S. indices, things went relatively well yesterday.

However, Europe closed slightly in the red, particularly in France and Germany, as both European heavyweights remain wary of what the U.S. president might unleash next regarding tariffs. Based on what he announced for Canada, Mexico, and China, it seems likely he’ll wait until markets close on Friday evening before making a move on the issue.

Europe mostly traded in the red, reflecting concerns over a potential American reaction. Additionally, Pernod Ricard expressed pessimism about its future outlook, stating that the economic, political, and geopolitical situation was too complicated to make any solid predictions. The spirits company has therefore decided to “navigate by sight and hope for the best.” Their gloomy comments, which gave the impression that management was in full burnout mode, weighed heavily on the stock, making it the biggest loser in the CAC 40 yesterday. But once again, the central question for European markets remains: “What is the orange man going to do next?” And more importantly, “How will our so-called leaders respond, given that they currently seem about as trustworthy as a group of drug dealers awaiting a shipment at a highway rest stop in southern France?”

But Wait, There’s More…

In short, Europe saw a slight decline, questioning what the next “Made in the White House” event would bring. Meanwhile, Valneva soared after announcing that the UK’s Medicines and Healthcare products Regulatory Agency (MHRA) had approved its iXchiq vaccine—the world’s first vaccine against chikungunya. This marks its fourth approval, following Europe, Canada, and the U.S. The stock jumped 17%.

And once again, I find myself wondering: why do scientists insist on giving vaccines such ridiculous names? In this case, “IXCHIQ”—six letters, only two vowels (which are the same), and four consonants, including a “Q” and an “X”! Seriously? Just trying to pronounce the vaccine’s name makes you feel worse than being bitten by a mosquito carrying chikungunya. They could have simply called it “the world’s most effective chikungunya vaccine” and saved us all some trouble. Okay, sure, it wouldn’t score as many points in Scrabble, but at least it would be pronounceable.

Elsewhere, TotalEnergies reported a 21% drop in profits for 2024. The company stated that market conditions were “less favorable” than in 2023. However, this bad news was already priced in, as the stock had fallen 30% from last year’s highs. The company forecasts oil at $70 per barrel in 2025, will continue investing in renewables, and wants to get listed in New York—without offending France. We’ll see how that works out.

TotalEnergies’ CEO also joined Bernard Arnault in saying that investing and growing a business in France is nearly impossible under the current tax and economic policies. Of course, that’s not exactly how he phrased it, but the message was clear. What’s interesting is that whenever Total posts record profits, the left-wing crowd gathers outside their headquarters, screaming for the CEO’s head because he isn’t handing out free money to every French citizen. But when profits are down—poof! Silence. Strange, isn’t it?

MAGA Mode Activated

Meanwhile, in the U.S., the conversation was quite different. The tariff issue was already forgotten. Investors have realized that Trump is using tariffs as a weapon of mass destruction to force trade partners into quicker negotiations—far more effective than hosting luxurious summits in five-star hotels where rooms cost $1,500 a night for a 24-square-meter room with a pool view.

So, instead of worrying about tariffs, the focus shifted to economic data and earnings reports. Yesterday, we got the first U.S. employment report under Trump 2.0—the ADP report. Now, we all know these numbers are basically meaningless because what really matters is the Non-Farm Payrolls report coming on Friday. But since yesterday’s ADP data showed strong job growth, it caught investors’ attention anyway.

According to the report, the private sector added 183,000 jobs in January. December’s numbers were also revised up, from 122,000 to 176,000. In short, better than expected, plus an upward revision.

Funny how that’s the exact opposite of what happened under Biden. Not saying there are two different calculation methods at play here, but… let’s just say I’m leaving that thought unfinished.

This stronger-than-expected job data immediately raised doubts about whether the Federal Reserve will cut rates anytime soon. Right now, the probability of a rate cut in March is at 16%. Thankfully, the bond market was more focused on the U.S. Treasury’s announcement that it won’t increase debt issuance in the coming months.