The U.S. markets ending in the middle of nowhere, Europe still being considered “cheap” by market participants, the DAX surpassing 22,000 for the first time in its HISTORY, and Powell confirming that there’s no rush to cut rates. This Tuesday, February 11, was another day following the same patterns as the past few days: an intense obsession with ARTIFICIAL INTELLIGENCE, tariffs dominating most conversations—along with Trump, Musk, and Vance. And in the end, Powell telling us nothing new, except that nothing has changed. Now, we’ll have to see if inflation will be a wake-up call for all of us.

From the Beginning

Since Donald Trump became the 47th President of the United States, we have been living to the rhythm of his explosive announcements. Since January 27, the world has been rocked by the declarations of a President whom some consider completely insane, while others believe he is bringing order to the world. It’s hard to take a side—especially since no one is asking us to. Nevertheless, we have to live with it. From now on, steel and aluminum will be taxed at 25%, starting in mid-March. This is no longer a surprise, and we have already been dealing with it for two sessions. The market, for its part, seems to be handling it reasonably well. However, the real question remains: how long can we ignore the actual consequences of these tariff increases, and what will be the next announcement? Who will be the next to take a hit?

For now, global indices seem immune. The performance of U.S. indices on Tuesday was unremarkable—we remain stuck in a sideways trading range, whether on the S&P 500, the Nasdaq, or the SOX. The only difference between these three indices is that the SOX has been stuck for much longer. It’s difficult to choose a direction when valuations are extremely high, yet shorting the market would be madness while the White House disruptor runs around telling everyone who will listen that he is going to restore America’s greatness, give every citizen a job, a home, and money—and, in a masterstroke, do it all without causing inflation to rise, or perhaps even lowering it.

Looking Forward to Tomorrow (Well, Today)

Yesterday’s session revolved around Trump’s statements, which no longer seem to scare anyone (for now). Beyond that, the market continued to hype artificial intelligence (thanks to the Paris summit), and as usual, investors kept buying into Germany and France because they’re cheap and breaking records daily. There was also time to analyze Coca-Cola’s earnings while waiting for Jerome Powell’s testimony before the nation’s top authorities. As for Coca-Cola, it outperformed market expectations, and Coca Zero sales pleasantly surprised investors. The stock had faced a tough previous quarter, but it looks like that’s behind them now. The share closed up nearly 5%, leaving behind a massive gap that may need to be filled someday—but let’s not spoil the celebration. As usual, Coca-Cola is a trend stock that should be bought when no one wants it anymore because, no matter what people say, it sells worldwide, and in the end, the bulls always win with Coca.

One of the other central themes of Tuesday was, of course, Jerome Powell’s testimony before the Senate Banking Committee. According to its chairman, the Fed has no reason to rush into cutting rates. He argued that the economy is “generally strong,” with a low unemployment rate, which does not justify immediate action. Not to mention that inflation remains above the Fed’s 2% target, which has existed since the dawn of time. The world’s top central banker explained to politicians—who spent the day questioning him about the new Trump administration—that he does not engage in politics. His job is to manage a real economy without worrying about his interviewers’ electoral concerns. He stated that the economy is broadly strong, has made significant progress toward its objectives, and that the Fed has absolutely no reason to rush into monetary policy adjustments. Notably, he specified “ADJUST” and not cut or raise rates—an intelligent way to keep a backdoor open just in case. His words were more or less, if not exactly, the SAME as those from the Fed’s January meeting.

In conclusion, Powell told the committee members and the rest of the world that “further rate cuts would depend on a MORE SIGNIFICANT decline in inflation AND the health of the labor market.” As for the labor market, there’s nothing to complain about (for now)—it remains strong. As for inflation, conveniently, it will be released this afternoon at 2:30 PM. Amusingly, Powell carefully avoided commenting on Trump’s new retaliatory measures and their potential impact on inflation—and, by extension, on a possible rate cut.

Inflation as the Target

So, as you’ve probably figured out, this Wednesday will be all about inflation—unless Trump or someone else decides to crash the party with a spectacular announcement. I don’t know, maybe a 25% tariff on Europe and 50% on France because Manu Macron didn’t greet Vice President Vance at the top of the Élysée Palace steps. Or maybe Musk announcing that he wants to buy Ford just to get their V8 engines and put them in Tesla S models to “Make American Automobiles Great Again.” Or Zuckerberg declaring that he wants to buy Hawaii and Nvidia because Meta has just logged its 17th consecutive day of gains.

Lately, macroeconomic fundamentals have often been pushed aside because people were too busy with other things. Remember last Friday’s job numbers? They generated about as much interest in the financial community as I have in the reproduction of clams on the southern coasts of New Zealand.

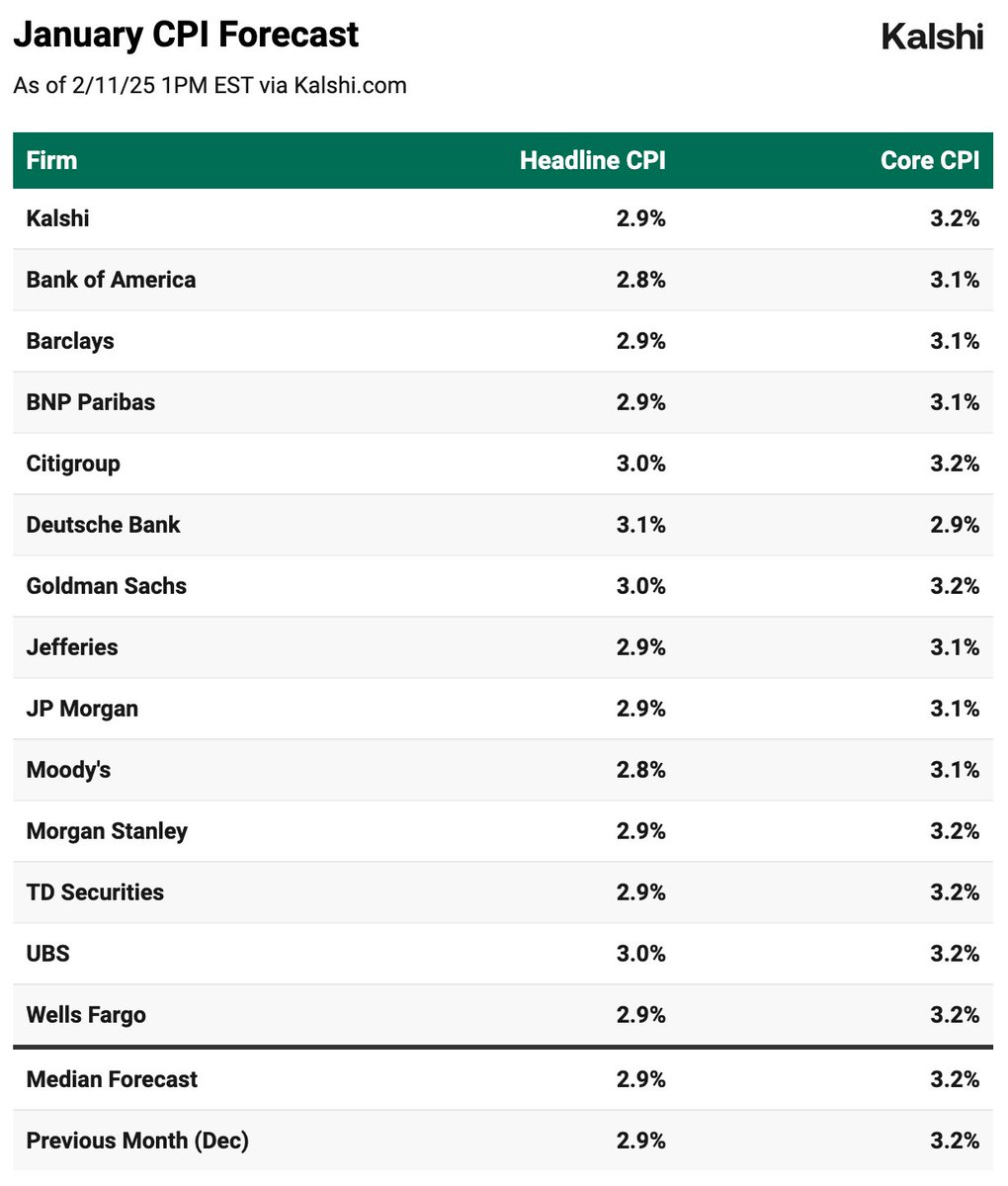

Regardless, this afternoon we’ll find out what inflation has done over the past 12 months and whether it has finally decided to come home, heading toward 2%. Looking at market expectations, CPI is expected to come in at 2.9%, and Core CPI (which only includes the stuff that’s doing well) is forecast at 3.2%.

For our personal knowledge, it’s worth noting that CPI hasn’t been above 3% since June 2024. If that happens today, the chances of a rate cut in 2025 would be as slim as my odds of winning the New York Marathon with a sprained ankle, broken glass in my shoes, and a 60-kilo sack of rocks on my back. In other words: ZERO chance—unless Trump orders it by presidential decree. Which, of course, is unconstitutional, but after all, the Constitution is there to be walked all over.

On the other hand, if CPI comes in at 2.8% or lower, it could be spectacular. And maybe, just maybe, the S&P could finally break out of its range. But I wouldn’t bet $10 on it.

CPI Estimate – Source: Kalshi.com

All in all, what we should take away from yesterday’s session is that Powell is waiting to see how inflation evolves, the market is waiting to see how inflation evolves, and also what Trump might do. Everyone is waiting to see what happens next, and since no one sees anything, I’m starting to think that buying a Labrador might be a good idea—at least to have a guide when we’re all wandering blind.

Now, Asia and Geopolitics

This morning, Asia is relatively calm, except for Hong Kong, which is up 1.5%. Notably, we’ve just learned that Baidu plans to launch the next generation of its AI model in the second half of the year. This information comes from an anonymous source close to the matter—not exactly the kind of news American AI companies want to hear. It aligns with Apple’s announcement yesterday about its collaboration with Alibaba to integrate AI into Chinese iPhones. The competition is heating up, and if it’s as fierce as BYD, which is giving Tesla a hard time with its DeepSeeeeeek integration in new autonomous models, there could be some concerns on the horizon. Tesla, by the way, got hammered AGAIN yesterday—both because of BYD and because everyone seems to hate Musk these days.

On the gold front, after nearly touching the holy grail of $3,000, the yellow metal stalled around $2,940 and has now pulled back, perhaps to gather strength for another jump. Currently, gold is at $2,910. Bitcoin is at $95,600 and isn’t looking great—we’ve seen better days for crypto.

However, we need to talk about oil. Crude prices have been climbing steadily for a few days. Even though there were some sellers last night due to slightly high inventory numbers, oil is still trading at $73 per barrel—compared to $70.43 last Thursday. It seems that geopolitical tensions in the Middle East are breathing new life into oil prices. After all, if Hamas doesn’t return the Israeli hostages by Saturday noon, Trump has threatened to break the ceasefire, and excavation work in Gaza will resume immediately. This flare-up in the region wouldn’t sit well with oil traders and could push gasoline prices up again.

The Rest of What You Need to Know

Beyond tariff policies, Musk’s daily ramblings, Tesla getting crushed every single day (now down 25% since the inauguration and completely oversold), Powell’s words, and the market’s CPI obsession, there were still some company earnings worth mentioning.

Let’s start with Kering. Yesterday morning, the other French luxury giant reported a 46% drop in operating profit, with a margin of 14.9% in 2024 compared to 24.3% in 2023. The numbers are ugly, and uncertainty still looms. What saved François Pinault from an even worse market reaction is that analysts expected even worse results. Gucci still isn’t doing well—it remains a mess (but that’s just my opinion). However, restructuring efforts continue, and there’s hope for improvement.

At Super Micro, it’s not just the market hoping for improvement—it’s the company itself. Yesterday, SMCI slashed its 2025 guidance and posted weaker-than-expected results, both compared to market expectations and its own. Initially, the stock got wrecked—down 10% during the session and another 10% after hours. But then, the company pulled a joker card—announcing it expects $40 billion in revenue for 2026, while the market had only expected $29 billion. This spectacular claim sparked a massive rebound, with the stock closing up 9% after hours. I’ll keep my thoughts on long-term forecasts for these kinds of companies to myself, but let’s just say I’m skeptical. Meanwhile, Super Micro still has to submit its financials to Nasdaq by February 25, which they claim will go smoothly. If you listen to their CEO, SMCI is back to being the fairytale stock it was before Ernst & Young walked out the door.

And finally, another earnings report worth noting—DoorDash. Last night, the company posted weaker-than-expected Q4 2024 profits, but the company that delivers cold meals in cardboard trays so you don’t have to get off your couch beat revenue expectations. And guess what our good old bipolar market decided to focus on? Yep, you got it! Revenue looked attractive enough to traders, and the stock soared 11% after hours. More revenue and more cardboard plates—I’m speechless.

Today’s Key Numbers

On the economic front, we have Powell’s testimony continuing and, of course, the CPI report—but I think you got that already. We’ll also get oil inventory data, which is expected to come in higher than forecast. And that’s about it.

On the corporate side, today’s earnings lineup includes Biogen, Cisco, Reddit, Robinhood, Heineken, and Schindler.

That’s all for this morning—I’m off to set my countdown timer. Catch you soon, but not tomorrow! Have a great day, everyone!