The past week has been spectacular. Spectacular because we have learned that we are no longer afraid of tariffs, no longer afraid of inflation, and with each passing day, we convince ourselves that artificial intelligence is the solution to all our problems. Not to mention that peace in Ukraine is just around the corner and that Trump is a fantastic accelerator of processes.

As for the markets, performance has been decent—Europe keeps climbing, while the U.S. is stalling at record highs. And this Monday, the States are closed. So why did we even show up?

Like a Monday

Mondays are never easy—coming to work is never simple, and getting back in front of the screens after the weekend is even harder. But it’s even more complicated when you have to come back to the office, knowing that the Americans are busy celebrating their Presidents and that their markets are closed. You know volumes will be lousy, and it’s likely to be too quiet. Yet, since the start of the year, all we’ve been hearing is that Europe is cheap, so we should buy. So maybe, this Monday without the Americans will be more exciting than usual—because Europe is cheap.

Honestly, I have no idea, but one thing is certain: with Trump returning to power, the divide between Europe and the U.S. has never been more pronounced. So, we’ll give European markets a chance in the absence of the Americans and hope that—who knows—since it’s a holiday over there, Trump might take the opportunity to rest, stay silent, and say nothing. Then again, the guy hasn’t stopped since January 26, and it feels like he never sleeps. The Americans used to have a President who seemed to be sleeping all the time, and now, with Trump 2.0, it feels like he never does.

Tariffs and Inflation

So, we’ll start the week gently, with low volumes, waiting to see what the market’s concerns will be. Given this sluggish start to the penultimate week of February, we’ll likely focus on the FOMC Meeting Minutes coming out Wednesday night—just to see if we missed anything from Powell’s closing speech. Though, to be fair, in his testimony before Congress last week, he already repeated the same thing. In short, the Minutes should be a non-event since we already know almost everything. But since there’s not much else to chew on, we’ll pretend it’s important.

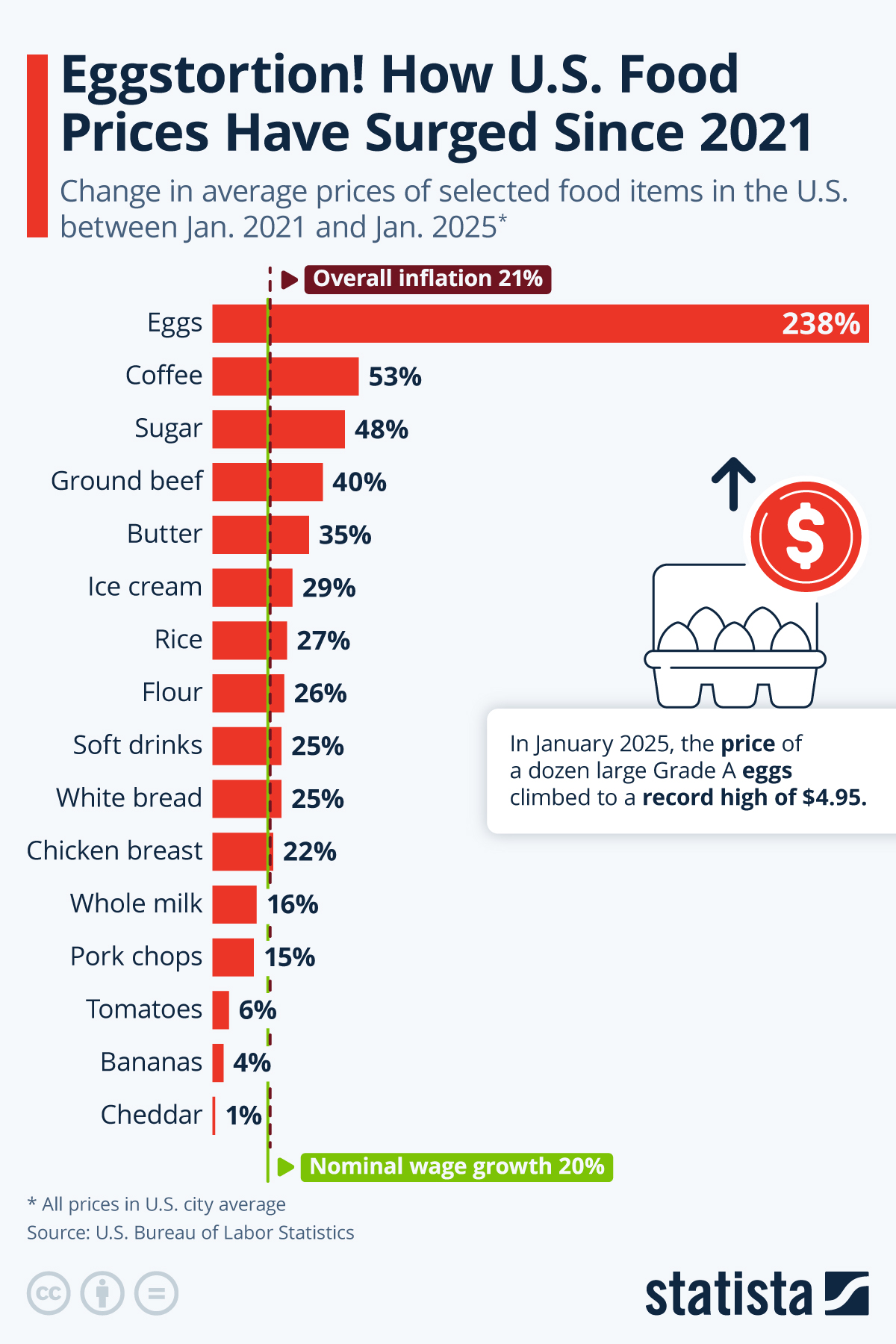

And since we have (too much) time this morning, we might as well ask ourselves how and why inflation went so unnoticed last week. There was actually reason to be concerned. We hadn’t seen it above 3% for more than eight months, the figure was well above expectations, and it’s clear that interest rates aren’t stopping prices from rising again. This immediately raises questions about the Fed’s next moves.

Questions

Because if inflation is rising while rates haven’t moved for weeks, we can ask ourselves:

(a) Is inflation climbing because rates aren’t high enough to stop people from borrowing and spending recklessly—especially since the economy is doing well and some Americans clearly still have money to spend?

Or (b), could this inflationary situation eventually push the Fed back to the “hawkish” side, forcing them to RAISE rates again? I know that’s not the narrative we’ve been sold since October 2023, but let’s face it—right now, inflation is no longer falling. Quite the opposite.

Yet, last week, the market didn’t flinch. In fact, the market doesn’t seem to care about inflation figures at all. After all, tariffs are no longer a concern, and Trump—the “dove of peace”—is supposedly about to end the war right under the noses of European leaders, who have poured half their GDP into Ukraine over the past three years.

When faced with such thrilling and disruptive news, it’s easy to forget the pesky issue of rising inflation. Plus, the media does a great job of reassuring us that, yes, inflation is climbing, but hey, it’s not that bad—so there’s no need to panic.

In reality, just when we thought we had buried inflation six feet under, it’s coming back stronger—more resilient than a zombie in The Walking Dead. And last week, we learned five essential things about why it refuses to die and return to Powell’s sacred 2% target.

Just Another Monday

Just Another Monday

Mondays are never easy—it’s never simple to get back to work, to sit in front of the screens again after the weekend. But it’s even harder when you know that the Americans are busy celebrating their Presidents, meaning their markets are closed, volumes will be terrible, and everything is likely to be way too quiet. Still, I don’t know, but since the beginning of the year, everyone keeps saying that Europe is cheap, so we should buy. Maybe this time, this Monday without the Americans will be more exciting than usual—because Europe is cheap.

Honestly, I have no idea. But one thing is certain: with Trump back in power, the gap between Europe and the USA has never been wider. So, let’s give European markets a chance in the absence of the Americans and tell ourselves that—who knows—since it’s a holiday over there, maybe Trump will take the opportunity to rest, stay silent, and say nothing. Then again, the guy hasn’t stopped since January 26, and it feels like he never sleeps. The Americans used to have a president who seemed to be sleeping all the time, and now, with Trump 2.0, it feels like he never sleeps at all.

Tariffs and Inflation

So, we’re starting the week slowly, with low trading volumes, waiting to see what the market’s concerns will be. Given this awkward start to the second-to-last week of February, we will likely focus on the FOMC Meeting Minutes coming out Wednesday night—to check if we missed anything after Powell’s closing speech. Although, since his congressional testimony last week was just a repetition of the same message, the Minutes are probably going to be a total non-event. We already know almost everything. But since there’s not much else to digest, we’ll pretend it’s important.

And since we have (way too much) time this morning, we can also ask ourselves why inflation flew under the radar last week. There was plenty to worry about—it had been over eight months since we last saw it above 3%, the figure was way above expectations, and it’s clear that interest rate levels aren’t stopping prices from rising again. This immediately raises the question of what the FED will do next.

Some Questions

Because if inflation is rising while interest rates haven’t moved for weeks, we have to ask:

(a) Is inflation climbing because rates aren’t high enough to prevent borrowing and reckless spending—especially since the economy is doing well and some Americans still have cash to burn?

Or (b) Could this inflation trend eventually force the FED back to the “Hawkish” side, leading to—wait for it—RATE HIKES?

I know this isn’t the narrative they’ve been pushing since October 2023, but right now, inflation isn’t dropping. Quite the opposite.

And yet, last week, the market didn’t flinch. The market doesn’t care about inflation figures. Why? Because in the meantime, tariffs are suddenly nothing to worry about, and Trump, “the dove of peace,” is apparently about to end the war in Ukraine—right under the noses of European leaders who have poured half their national GDPs into Ukraine for the past three years.

When faced with such groundbreaking, disruptive news, it’s easy to forget that inflation is creeping back up. And, of course, the media is helping us understand that, yes, inflation is rising—but it’s not a big deal. So, no need to panic.

A Strong Economy = Inflation Guaranteed

The Fed went all in, hammering interest rates to cool down the overheated economy. The result? Unemployment is still low, people keep spending their money, and inflation is bouncing back like a trampoline. Apparently, consumers didn’t get the memo that things were supposed to slow down and that it would be great if they could cut back on spending.

The problem is always the same: when you have money to burn—and when you’ve been coached your whole life to “spend, baby, spend”—it’s hard to stop.

Services Cost a Fortune

Prices on high-tech gadgets have stabilized a bit, but Americans have shifted their spending to vacations, restaurants, and overpriced insurance. And since no one takes out a loan to go to dinner or get their back waxed, the Fed is powerless against this spending frenzy. It’s clear—services are driving inflation higher. People may be holding back on buying physical goods, but since there’s nothing wrong with a little self-indulgence, they’re getting massages instead.

Inflation Is Already in the Pipeline

Commodity prices are skyrocketing faster than a SpaceX rocket. Oil, wheat, cocoa—everything is going up. Add new tariffs on steel and aluminum to the mix, and you’ve got the perfect Molotov cocktail to fuel inflation for quite some time.

Tariffs? No Panic Yet, But…

Companies are sweating as Trump waves the threat of a new trade war. So far, everything is fine, but they’re staying on high alert. The plan? Be ready to pass increased costs onto consumers—just like always. After all, nobody wants to absorb the extra costs of inflation, so why not let the consumer pay for it instead?

January: The Most Deceptive Month

Ah, January—the month when companies hike prices to start the year off right. This completely skews the numbers, but economists smooth it all out. The problem? When they get it wrong, the indicators end up looking scarier than reality.

Conclusion? We’ll have to wait a few more months to get a clearer picture before deciding whether to panic (or not).

In short: The Fed is struggling, inflation is holding strong, and everyone is holding their breath.

To be continued…

In Asia This Morning

This morning, Asia is open—no “Presidents’ Day” here. Movements aren’t spectacular; everything is slightly up, and the only real takeaway is that Japan’s GDP came in strong. Maybe a little too strong. Because when it’s too good, fears of a rate hike in Japan start creeping back in. We’ve been talking about it for a while now, and it feels like the guillotine blade is getting closer.

Elsewhere, gold is at $2,910, oil is battling around $70, and Bitcoin is at $96,500.

Today’s Headlines

Rumors are circulating in “well-informed circles” that Taiwan Semi and Broadcom are separately considering buying out Intel—then breaking it up. Broadcom is eyeing Intel’s design division but won’t make a move unless it finds a partner for manufacturing. TSMC, on the other hand, is interested in the factories, potentially through a consortium. No alliance between the two—just separate discussions—but the idea of a fragmented Intel has never seemed more credible. Once untouchable, the tech giant might soon have to choose: manufacture or design—but not both. The beginning of the end? Maybe. The beginning of a breakup? Probably. At least, that’s what The Wall Street Journal suggested this weekend.

Meanwhile, Emmanuel Macron, the divine patron saint of Europe, has called for an emergency meeting of European leaders to discuss how to take part in talks on Ukraine—without looking (too) ridiculous. And maybe, just maybe, to figure out whether they actually want the war to end.

On the other side, the Ukrainian leader declared this weekend that Putin’s ultimate goal is to declare war on NATO. Which is ironic, considering we’re constantly told that Russia is on its last legs, completely crippled by sanctions. Yet somehow, at the same time, they’re allegedly preparing to take on NATO head-on.

In Short

This morning is quiet. U.S. markets are closed, there are no major economic reports, and the week doesn’t really start until tomorrow. But given the current enthusiasm for European stocks, we might still be in for some surprises!

Have a great day, and see you Tuesday morning. In other words: See you tomorrow!