While awaiting information on the discussion between Trump and Putin regarding the division of Ukraine, markets are holding back ahead of meetings of various central banks: the U.S. Federal Reserve and the Bank of Japan on Wednesday, followed by the Bank of England and the Swiss National Bank (SNB) on Thursday. Meanwhile, the Empire strikes back. The Canadian Prime Minister is in Paris before meeting with leaders from other European capitals.

A bit of economics…

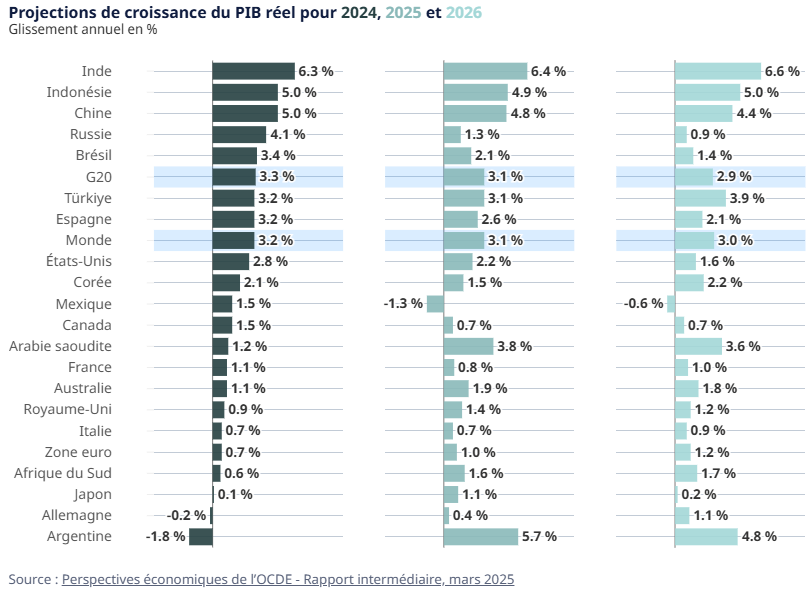

The global economy remained resilient in 2024, with a robust 3.2% annualized growth rate in the second half of the year. However, recent activity indicators suggest a moderation in global economic growth prospects. Business and consumer confidence have deteriorated in some countries. Inflationary pressures persist in many economies. At the same time, uncertainties regarding public policy remain high, and significant risks persist. The continued fragmentation of the global economy is a major source of concern. Higher-than-expected inflation would lead to a more restrictive monetary policy and could result in disruptive price corrections in financial markets. Conversely, agreements to lower tariffs from their current levels could boost growth.

The OECD now expects global growth to reach 3.1% in 2025, down from 3.3% in its previous December projections. The United States, where President Donald Trump has sparked a trade war with key partners, is projected to see its GDP grow by 2.2% this year, before slowing to 1.6% next year, according to the OECD, which has thus lowered its growth forecasts for the country by 0.2 and 0.5 percentage points, respectively.

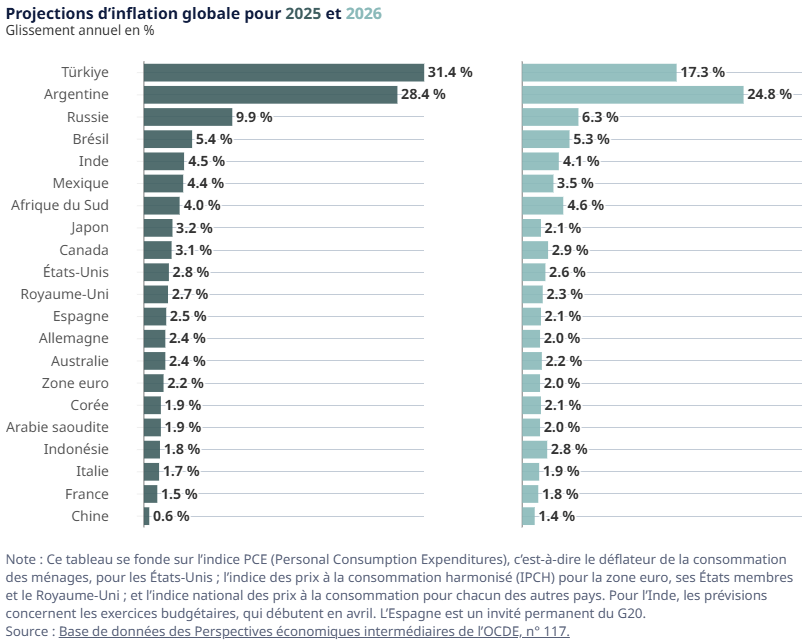

OECD experts expect inflation to accelerate to 2.8% in the United States this year (+0.7 percentage points compared to their previous forecast), after 2.5% in 2024.

A Bit of Trump… As Usual

Why is Canada in the crosshairs of the American president? Oil, base metals? Well, according to Tricia Stadnyk (The Conversation, March 13, 2025), Trump wants to put some water in his Californian wine. Explanation. The United States’ interest in Canada’s water is concerning, even though it is not new. Recently, the U.S. halted negotiations on the Columbia River Treaty, a key agreement on water sharing between the two countries. Geopolitical tensions, combined with demand outpacing supply in a context of climate change, pose an imminent and very real threat to Canada. A long-abandoned water project, known as the North American Water and Power Alliance (NAWAPA), was initially proposed by the U.S. Army Corps of Engineers in the 1950s. It is considered a “zombie project” that keeps resurfacing but never truly dies. It is no coincidence that water is referred to as “blue gold.”

And What About the Markets?

European stock markets ended higher as the U.S. economy confirmed its slowdown, just two days before the Fed meeting. The CAC 40 index gained 0.57% to 8,073.98 points, while the EuroStoxx50 rose 0.69% to 5,441.46 points.

In Switzerland, ahead of the Swiss National Bank (SNB) decision next Thursday, the SMI closed up 1.09%. Novartis rebounded and gained 2.3%. The other pharmaceutical heavyweight, Roche (+1.7%), also supported the index, as did Nestlé (+1.2%), though to a lesser extent.

German bond yields fell after reaching their highest levels since October 2023, following the debt brake reform agreement in Germany. The downward revision of Germany’s growth forecasts by the Ifo Institute also contributed to lower yields. The 10-year German Bund yield fell by 7.1 basis points to 2.8030%, while the 2-year yield ended the session slightly lower at 2.1810%. In France, the 10-year OAT yield dropped 9 basis points to 3.4780%.

In the United States, the picture was more mixed. The Dow Jones advanced 0.85%, the Nasdaq gained 0.31%, and the broader S&P 500 rose 0.64%.

- Chevron, the American oil giant, gained 1.08% after announcing the purchase of about 5% of Hess Corporation’s shares.

- Intel surged 6.82% after documents revealed that its new CEO, Lip-Bu Tan, had purchased $25 million worth of company shares.

- The 10-year U.S. Treasury yield increased by 0.6 basis points to 4.314%, compared to 4.308% last Friday.

- The 30-year U.S. bond yield fell by 1 basis point to 4.6045%, from 4.615% on Friday evening.

- The 2-year U.S. bond yield increased by 4.4 basis points to 4.059%, compared to 4.015% on Friday night.

Foreign Exchange Market

The euro, which has strengthened in recent sessions due to hopes of a German budget agreement, was up 0.4% at $1.092. It was near its $1.0947 peak from last week, the highest level since October 11.

The dollar rose 0.4% against the yen, reaching 149.160 yen, close to last week’s low of 146.52 yen.

Meanwhile, the Chinese yuan approached its four-month high in offshore trading, trading at 7.233 per dollar.

In cryptocurrencies, Bitcoin was up 1.6% for the day at $84,552.

Commodities

- Spot gold was up 0.2% at $3,008.08.

- Spot silver gained 0.2%.

- Platinum added 0.5%, and palladium increased 0.5%.

On the London Metals Exchange (LME):

- Copper remained at its five-month high of $9,864 per ton, driven by China’s stimulus plan and a weaker U.S. dollar.

- Aluminum remained stable.

- Lead dipped 0.1%.

- Zinc lost 0.2%.

- Tin declined 0.5%.

- Nickel fell 0.8%.

Oil Prices

Oil prices rose on Monday after the United States reaffirmed its commitment to relentlessly attack the Houthis in Yemen. Additionally, China’s economic data released earlier in the day fueled hopes of higher demand.

- Brent crude increased 0.43% to $70.88 per barrel.

- West Texas Intermediate (WTI) crude gained 0.31% to $67.39 per barrel.

Agricultural Commodities

- Wheat futures in Chicago surged on Monday, as windstorms in U.S. grain regions raised fears of crop damage. Analysts also noted that traders expect a decline in Russian exports, which could increase demand for U.S. wheat.

- Soybean prices fell due to lower-than-expected production figures.

- Corn prices edged slightly higher.

This Morning in Asia

The Hang Seng was up 2% in morning trading, and its 23% gain since the beginning of the year is the largest among major financial markets.

Mainland Chinese stocks recorded more modest gains, while the MSCI Asia-Pacific index rose 1%, with markets in Seoul, Sydney, and Taipei also posting gains.

The Nikkei rebounded by 1.5%.